Carrier Vetting for Risk Exposure 101

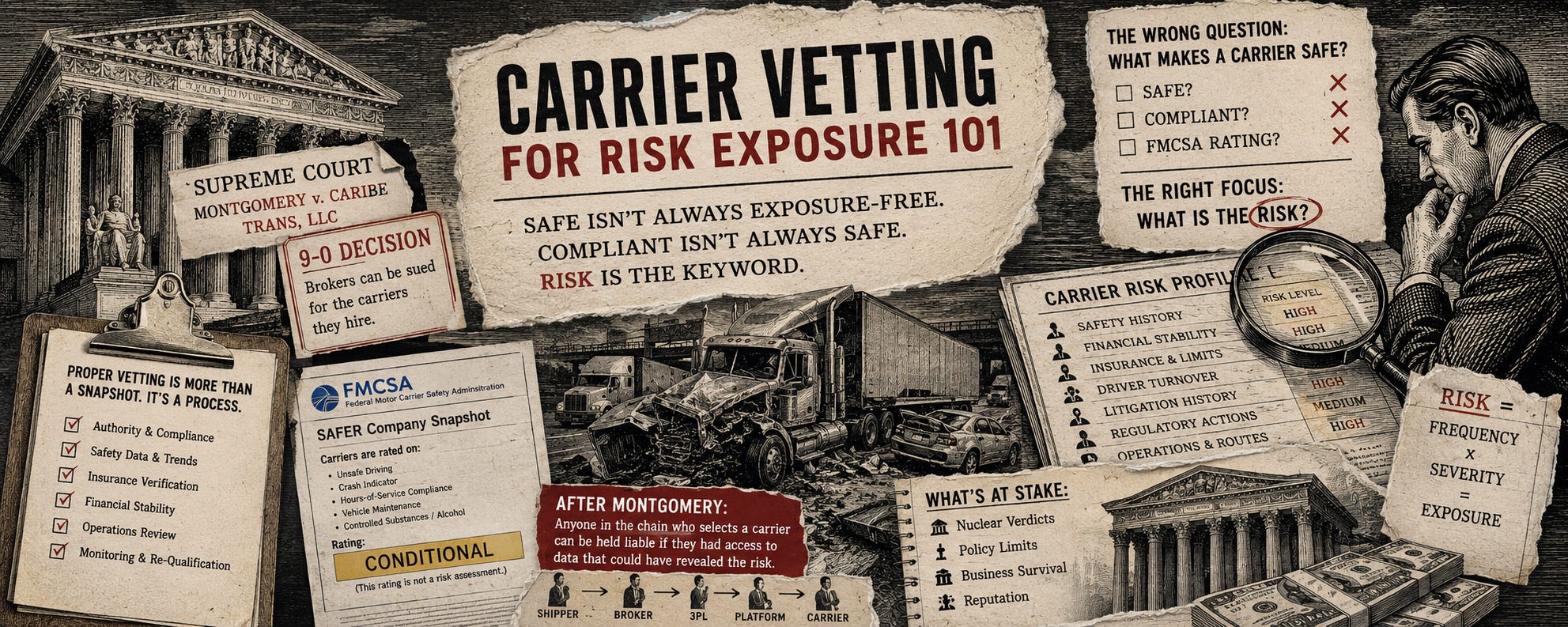

Safe isn’t always exposure-free or risk-free. Compliant isn’t always safe. What “safety” means doesn’t matter. Risk is the keyword.

Since the Supreme Court handed down Montgomery v. Caribe Transport on May 14, I have not been able to get through a phone call, a deposition prep, or a LinkedIn thread without somebody asking me the same question. What makes a carrier safe? If we cannot just lean on FMCSA’s SAFER snapshot anymore, what is the objective standard? Where is the line?

These are the wrong questions, and I want to spend some time here explaining why, and then walking through the questions we should be asking instead. Consider this a primer. A 101 because the industry has been operating on a definition of carrier vetting that was never actually correct, and after Montgomery, the cost of that mistake just went up for everyone in the chain.

Here is the quick refresher on what the Court did, because the rest of this depends on it. The justices ruled 9 to 0. Justice Amy Coney Barrett wrote the opinion. Justice Brett Kavanaugh filed a concurrence joined by Justice Samuel Alito. The plaintiff, Shawn Montgomery, lost part of his leg in 2017 when a Caribe Transport truck struck his parked tractor-trailer on an Illinois shoulder. C.H. Robinson brokered that load. The carrier, Caribe, carried a conditional safety rating at the time. The Court held that the Federal Aviation Administration Authorization Act does not preempt a negligent selection claim against the broker, because the statute’s safety exception saves it. For roughly a decade, brokers leaned on FAAAA preemption to get these cases dismissed before discovery ever started. That shield is gone.

The principle the Court announced is that exercising ordinary care when you select a carrier concerns motor vehicle safety. That logic reaches shippers who pick carriers directly. It reaches third-party logistics providers. It reaches digital freight platforms. Anybody in the chain who selects a carrier and who has access to the public safety data is now exposed.

Three words that are not synonyms

Here is the first thing I want to fix, because almost every conversation I have about this runs aground on it. Safe, compliant, and risky are three different words, yet the industry uses them as if they mean the same thing. They don’t.

Compliant means a carrier meets the minimum standard the federal government will accept before it lets that carrier keep its operating authority. Compliance is a floor. It is pass-or-fail, and the bar is set low on purpose because the Federal Motor Carrier Safety Regulations are a national minimum, not a best practice. When a carrier is compliant, what you actually know is that on the day somebody checked, that carrier was not so far out of line that the government would pull its authority. That is it. That is the whole guarantee.

Safe describes an operational outcome. Did the truck get from point A to point B without hurting anyone or damaging the freight? Safe is a track record. It is backward-looking and mostly a function of things hard to see from the outside: driver behavior, equipment condition, dispatch pressure, fatigue, and the weather that day.

Risk is the one VERY FEW define because for most, it’s not what they do, yet it is the one that matters. Risk is exposure. Risk is the amount of financial and human damage a carrier is capable of causing, the likelihood it will cause it, and who pays when it does. Risk is forward-looking. It is probabilistic. Critically, it includes an entire category of factors that have nothing to do with safety or compliance.

Here’s what people miss. A carrier can be compliant and unsafe. A carrier can be safe and out of compliance on paper. And a carrier can be both safe and compliant and still be a genuinely bad risk. After Montgomery, when that carrier causes a catastrophic crash, safe-and-compliant is not the shield people think it is, because the plaintiff’s lawyer is not going to argue compliance. He is going to argue risk, and he is going to argue that you could have seen it coming.

Risk 101: frequency and severity

If you have ever sat across the table from an underwriter, you already know how they think, even if they never said it out loud. Risk has two axes. Frequency and severity. How often something bad happens, and how bad it is when it does.

Frequency multiplied by severity gives you expected loss. That is the actuarial spine of every commercial auto premium ever written. An underwriter is not really asking if this carrier is safe. The underwriter is asking, over the policy period, how many losses am I likely to see, how big are they likely to be, and what is the tail? The tail is the rare, catastrophic, company-ending event. The multi-fatality crash. The hazmat release. The nuclear verdict. This is why insurance has multiple risk layers, especially in captive groups.

There is no line item for safety rating. There is no field for compliant, yes or no. Those things might correlate loosely with frequency. They tell you almost nothing about severity, and severity is where companies die.

There is one more distinction worth keeping straight, because it is the difference between the people who do this for a living and the people who think a SAFER printout is due diligence. A hazard is a source of potential harm. Risk is the probability that the hazard will actually cause harm, multiplied by the severity of that harm. Exposure is how much of your value, or your client’s value, is standing in front of that risk when it goes off. When an insurer retains me to assess a fleet, I am not grading the fleet’s character. I am estimating frequency, estimating severity, and pricing exposure. That is the lens. Carrier vetting, done correctly, is the exact same lens applied to a hiring decision rather than a policy.

The FMCSA data trap

So let’s talk about the data the whole industry actually leans on, and what it does and does not tell you.

FMCSA assigns exactly three safety ratings, and only after an on-site compliance review. Satisfactory means the carrier had functional safety management controls on the day of the audit. Conditional means the auditors found those controls inadequate. Unsatisfactory means the carrier is unfit and must stop operating within a short window. That is the entire scale.

Roughly 92 percent of carriers have no rating at all. They are Unrated. Out of something like 780,000 motor carriers in this country, the overwhelming majority have never had an auditor walk through the door. FMCSA has never had the investigators rate them all, and it does not now.

So when a broker or a shipper pulls up a carrier and the rating field says Unrated, that does not mean safe. It means nobody from the federal government has looked. Some unrated carriers are small, disciplined, well-run operations that have simply never come up in the audit lottery. Others are problems waiting to be discovered. From the rating alone, you cannot tell which is which, and that is the trap. The absence of a bad rating gets read as a good rating. It is not one. Unrated is not a clean bill of health. It is an empty file.

Satisfactory has its own problem: time. A satisfactory rating can be six, eight, or ten years old. It reflects the carrier that existed on audit day. Fleets turn over. Owners sell. Safety directors leave the program behind. A satisfactory rating from 2017 tells you about a company that may no longer exist, and the rating field will not tell you how old it is unless you look.

Conditional is the rating that actually carries weight, and it carries it in the wrong direction. A conditional rating indicates that the FMCSA has already found serious deficiencies. If you hire a conditional carrier and it is involved in a crash, you are going to be explaining to a jury why you chose a carrier that the federal government had formally flagged. That was the exact fact pattern in Montgomery. Caribe carried a conditional rating. That is not a coincidence in this case. That is the case.

Conditional ratings cost money even when nothing goes wrong. Carriers with a conditional rating typically see commercial insurance premiums run 15 to 40 percent higher, are excluded from many shipper- and broker-approved lists, and lose access to most government freight. The market already prices conditional as a risk. It just does not have a clean way to price everything that the rating leaves out.

That is the core problem with leaning on SAFER as your vetting standard. It is a thin, lagging, mostly empty dataset that was never built to measure exposure. It was built to help FMCSA triage which carriers to investigate with limited resources. The industry borrowed it as a hiring tool because it was free and readily available. Free and there is not the same as adequate.

The 360-degree view and what actually goes into a risk profile

If FMCSA data is a thin slice, what is the whole picture? What does a real 360-degree carrier risk profile actually include?

This is the question I set out to answer when we built Tea Technologies and the CarrierVerifi platform. We did not build it the way you build a compliance checker. We built it the way I think an insurer or a litigator would when they retain me to assess a fleet, because that is the actual job, and the job has very little to do with checking boxes. This is the platform FMCSA special investigators use today.

Start with financial health. We integrated SEC EDGAR for publicly held carriers and their parent companies because a carrier’s balance sheet is a non-FMCSA leading indicator of risk that is not reflected in safety regs. A carrier under financial stress makes predictable choices. It defers maintenance. It stretches trade cycles on tractors and trailers past where they should. It cancels the telematics subscription. It lets the safety director position sit empty for a year. None of that shows up as a violation until after it shows up as a crash. The money is upstream of the safety data.

Then culture. We pulled in OSHA inspection and violation history, because how a company runs its shop, its dock and its yard tells you how it runs everything else. A carrier that cuts corners on a machine guard or a fall hazard in the shop is telling you something true about how it thinks about risk on the road. Culture is the single largest driver of loss, and there is no FMCSA field for it anywhere.

Then the corporate structure. We tied in OpenCorporates, because who a carrier is connected to changes the risk picture completely. Shared officers. Shared addresses. Shared phone numbers. A pattern of authorities opened and closed. This is how you surface a chameleon carrier, an operation that lets a bad authority die and reincarnates clean under a fresh DOT number. In a safety snapshot, a chameleon looks brand-new and therefore harmless. In a corporate tie analysis, it looks like exactly what it is.

Then, the litigation history. We tied in federal court records, because a carrier’s litigation footprint is one of the loudest risk signals there is, and almost nobody looks at it before tendering a load. If a carrier has 350 trucks, five years of operating history, and a couple of hundred federal cases spanning wrongful death, personal injury, employment claims and civil rights complaints, no BASIC score is going to tell you what those dockets tell you. Litigation is the system already scoring the carrier’s risk for you. You just have to go read it. If you hire that carrier, these federal litigation cases are the cases you could now be exposed to.

Then catastrophic exposure. We added PHMSA incident data across all available history, because a hazardous materials release is the textbook tail risk. Low frequency, brutal severity, and very capable of ending a company and pulling its broker and shipper into the claim.

We even brought in U.S. Census data, because regional and demographic context, local crash rates and the economic conditions where a carrier is domiciled and runs its lanes, move real-world exposure whether the industry likes it or not.

That is more than 30 integrations now, and almost none of it is compliance data. Most of it is not safety data. It is risk data. It is the material that does not appear in a SAFER snapshot and that still decides outcomes anyway. The reason most carrier vetting does not look like this is not that the data is hidden. It is public. The reason is that very few people in this industry have actually sat in the loss control chair. There are a lot of compliance people. There are a lot of safety people. There are very few fleet risk professionals trained to look at the entire board at once.

How to actually vet, qualify and screen a carrier

All right. Here is the part that earns the 101 in the title. If safety ratings are not the standard, what is the actual process? How do you vet, qualify and screen a carrier so that the decision holds up, both on the road and later in a deposition?

Think about it in three phases. What you do before you ever tender a load. What you do to make the process itself defensible? And what you do after, because vetting is not a one-time event.

Phase one is the pre-tender screen, and it has more layers than most operations actually run.

Authority and identity come first. Confirm the carrier actually holds active operating authority for the type of freight you are moving, and confirm it through live FMCSA data, not a number somebody emailed you and not a stale record in your own system. This is also where you catch double-brokering and identity theft, which are no longer edge cases. Verify that the carrier you are talking to is the carrier on the authority. Match the MC and DOT numbers, the legal name, the phone number and the email domain. A carrier calling from a free email account that does not match the registered entity is a flag, not a formality.

Authority age is next, and it is one of the most useful and most ignored signals there is. A carrier with operating authority less than 12 to 18 months old is a new entrant. New entrants are not automatically bad, but they are statistically higher risk; they have not yet undergone their new-entrant safety audit, and the post-Montgomery trade coverage specifically named authority under 18 months as one of the markers plaintiff attorneys are building case files around. Brand-new authority is also the calling card of the chameleon carrier. New authority is not disqualifying. It is a reason to look harder, not a reason to look away.

Insurance is where a lot of vetting is technically done and substantively useless. Pulling a certificate of insurance is not verification. The certificate has to be current, the coverage limits have to actually fit the load and the exposure, and the smart move is to get that certificate directly from the insurance agent rather than from the carrier, because a certificate is a document and documents can be edited. Confirm the policy is genuinely in force, not lapsed and not pending cancellation. Require yourself as an additional insured and a waiver of subrogation where appropriate. And understand the limits problem in plain terms. The federal minimum for most general freight is still 750,000 dollars in auto liability, a number set decades ago that would not come close to covering a single serious injury today, let alone a fatality. A carrier carrying only the federal minimum is not adequately covered. It is legally compliant and financially exposed, and after Montgomery, that exposure flows straight up the chain to whoever selected it.

Safety performance comes next, and this is where you read the FMCSA data correctly instead of superstitiously. Look at the safety rating, but date it and discount it accordingly. Look at the BASIC percentiles in the Safety Measurement System, but read them in context. A high Unsafe Driving or Hours of Service percentile is a different and more serious problem than a high percentile in a paperwork-heavy category, and percentiles have to be read against the size of the carrier and the number of inspections it has had. Look at the crash history, and do not just count crashes. Weight them. A fatal is not a tow-away. Look at preventability where it is available. Look at the out-of-service rates for both drivers and vehicles against the national averages, because OOS rates are one of the better near-real-time behavioral signals FMCSA gives you for free.

Then go past FMCSA entirely, which is the whole point of the 360 view. Pull the financial picture if the carrier has one. Run the corporate-tie analysis to surface chameleon patterns and connected entities. Pull the federal litigation footprint. Check PHMSA to see if there are any hazmat dimensions at all. This is exactly the work CarrierVerifi was built to consolidate, because doing it by hand across a dozen separate public systems for every carrier you touch is not realistic, and not realistic is not a defense a jury is going to accept anymore.

Phase two is making the process itself defensible, and this is the part Montgomery changed most directly.

Have a written carrier vetting standard operating procedure. Put it on paper. Define the minimum criteria. Define what raises a flag. Define who is allowed to override a flag and what they must document when they do. Then follow it the same way every single time. The reason this matters is not bureaucratic. In discovery, the first thing a plaintiff’s attorney is going to request is your carrier vetting policy and the file on the carrier that crashed. If you have a written SOP and a documented file showing you followed it, you have a defense. If you have no SOP, that absence is itself evidence. An undocumented process and a nonexistent process look identical from the outside, and a jury will treat them the same. Vet consistently, and write down that you did it.

Phase three is continuous monitoring, because a carrier’s risk profile is not a photograph. It is a film. The carrier you vetted in January can have a lapsed insurance policy, three new crashes and a downgraded rating by June. So track certificate-of-insurance expirations and set a hard rule: do not tender to a carrier whose coverage has gone inactive. Monitor the carrier’s FMCSA Safety Measurement System data on a recurring basis, and flag movement, not just absolute scores. A carrier whose violation trend is climbing is a materially different risk than the same carrier with the same scores trending down, and the trajectory is something almost no vetting process ever looks at. This is the logic behind the monthly FMCSA monitoring we built into TruckSafe Risk Control’s process. You are trying to catch deterioration while it is still a data point, before it becomes a claim, and well before it becomes a verdict.

Put it in the contract. A master transportation agreement should include a hold-harmless and indemnification structure, an insurance and additional-insured requirement, a clear delegation of cargo securement responsibility, and an explicit prohibition on re-brokering the load without your written consent. The no-re-brokering clause matters more than people think, because the moment your vetted carrier quietly hands the load to an unvetted one, every bit of diligence you did is worthless, and you may not even know it happened until the crash report names a carrier you have never heard of.

The driver layer: where the floor is not the standard

Everything above is carrier-level. There is a driver-level version of the same problem, and it follows the exact same pattern. Compliance sets a floor, and the floor is not where risk lives.

Take the motor vehicle record. To be compliant, a carrier pulls a driver’s MVR at hire and once a year after that. FMCSA says that is enough. Is it enough for you? It is not. A once-a-year MVR means a driver can pick up a serious violation, a suspension, even a DUI in February, and the carrier does not find out until the following January, if it finds out at all. There are continuous license monitoring services, SambaSafety and other providers, that watch the record every day and alert the carrier the moment something changes. That is not a compliance requirement. It is a risk control. The questionnaire we use in our assessments asks specifically whether a carrier runs continuous license monitoring and, just as importantly, whether it acts on the alerts within 24 hours, because a monitoring service nobody reads is theater.

Take the Pre-Employment Screening Program. Pulling a PSP report is not required. But PSP shows a driver’s actual roadside inspection and crash history across previous employers. A carrier that does not run PSP is choosing not to see information that is sitting right there for the asking. In litigation, choosing not to look is its own kind of finding.

Take the road test. To be compliant, a carrier can decide that a valid CDL is proof enough and skip the behind-the-wheel road test entirely. Then there is a crash. And the question in front of the jury becomes this. Did you really decide that ten minutes’ ride to confirm that this person could actually operate this truck was too much to ask before you put him next to my client’s family? That is the question. That is the hole. It has nothing to do with whether a box was checked and everything to do with risk.

Take the Drug and Alcohol Clearinghouse. Compliance is running the query. Risk control is what you do with a hit: how fast your designated employer representative reports it, whether you have a real return-to-duty process, and whether your random testing pool is genuinely maintained as drivers come and go. The gap between the minimum and the defensible standard is, once again, the entire point.

What a real 360 assessment actually asks

When TruckSafe Risk Control runs a risk control assessment on a fleet, it is not a compliance review, and the difference shows up immediately in the questions. We use a structured risk control questionnaire that runs roughly 120 questions, and a large share of them have nothing to do with whether a driver can physically operate a commercial vehicle. They are not safety questions. They are not compliance questions. They are risk questions. I want to give real examples because they make the distinction concrete.

In the governance section, we ask whether annual risk-reduction goals are built on leading indicators, things like BASIC percentiles, out-of-service rates and claims frequency, rather than lagging ones. We ask whether, at a multi-terminal carrier, loss costs are charged back to the local profit-and-loss statement, because a terminal manager who never feels the cost of a claim will not manage to prevent it. We ask whether safety budgets are approved and tracked at the executive level, and whether supervisors are evaluated on safety metrics in their annual reviews. None of that is in the Federal Motor Carrier Safety Regulations. All of it predicts loss, because it tells you whether safety is a line item with a budget and an owner, or a poster on a wall.

In the vendor and contracted-transport section, we ask whether the carrier has a written carrier and broker vetting SOP of its own, whether it tracks certificate-of-insurance expirations and blocks a tender when coverage lapses, whether its owner-operator lease actually specifies maintenance, equipment age, insurance and driver criteria, and whether subcontractor pay is tied in any way to safety performance. That last one tends to surprise people. It is a question about how a company spends its money, and it is one of the better predictors of how seriously it takes supply chain risk.

In the emergency response section, we ask whether the carrier has a crisis-management and media plan for a high-profile crash, whether each vehicle has an accident kit with a camera, and whether incident investigations are conducted within 24 hours using a real root-cause methodology. The first 24 hours after a catastrophic crash largely determine the litigation trajectory, and a carrier that has never thought that through is telling you something important about itself.

In the claims and continuous-improvement section, we ask whether quarterly loss-trend reports actually drive new safety initiatives, whether there is an annual management review of the carrier’s own risk score and action plan, and whether the policy manual has a maintained revision history. A revision history sounds like a clerical detail. It is not. It is the difference between a living program and a binder somebody bought once and never opened again.

Then we do the thing that turns it from a survey into an assessment. We make the carrier upload its actual policies, the specific ones, not a table of contents. If a policy does not exist, that absence is a finding. Then we weigh the carrier’s answers against its FMCSA history, because the federal record tells us whether the carrier is actually managing the program it just described or simply knows the right answers to give. A carrier can tell you it has a robust fatigue management program. Its Hours of Service violation history will tell us whether that is true. Then we layer in the claims and loss-run history, because if the losses do not match the program, the program is fiction. We are cross-referencing what the fleet says against what the federal record and the loss data show, and the contradictions are where the real risk profile lives.

That is what a 360-degree view actually means. It is not more compliance. It is a different question entirely, asked with the data to check the answers.

The litigation reality

I have referenced the courtroom a few times, so let me put real numbers on why this is real.

A nuclear verdict, in the shorthand the insurance and trucking world uses, is a jury award of over $ 10 million. According to the American Transportation Research Institute, the median nuclear verdict reached roughly 36 million dollars in 2022, about 50 percent higher than a decade earlier, and mean verdict awards have been climbing at better than 50 percent a year, far outpacing both general inflation and healthcare costs. The U.S. Chamber of Commerce, reviewing truck-crash settlements and verdicts over a recent three-year period, found average awards in the range of $ 27 million. Verdicts over $ 50 million are a growing share of the total each year.

The mechanism behind many of those numbers is what defense lawyers call the reptilian theory. The plaintiff’s attorney does not really try to prove the accident. He tries the company’s character. He is not in that courtroom to prove the driver was three miles an hour over the limit. He is there to convince the jury that the company is an ongoing danger to that juror’s own family and community, and that the only responsible response is a verdict large enough to send a message. The way you build that narrative is by finding holes. The road test that was skipped. The MVR that was pulled once and filed. The carrier that was sourced because a screen said Satisfactory. Reptile theory runs on the gap between the minimum a defendant met and the standard a reasonable person would expect, and the wider that gap, the bigger the number.

The environment for it keeps getting more hostile. Swiss Re’s research found that 76 percent of U.S. consumers now believe jury awards are too low, and among adults under 40, that figure climbs to 83 percent. Those are the people filling jury boxes. ATRI has also tracked third-party litigation funding, in which outside investors bankroll these suits in exchange for a share of the award, which has grown several hundred percent in just a few years. That funding removes the financial pressure that previously pushed plaintiffs toward an early, smaller settlement.

Here is what Montgomery added to it all. Before May 14, in most of the country, the broker had a strong shot at getting out of the case early on preemption grounds, and the verdict, if it came, would have landed on the carrier. After May 14, the negligent selection claim against the broker survives, the broker undergoes full discovery, and the verdict can be apportioned among the carrier, the broker, and, by the same legal logic, the shipper. A 40 million dollar verdict is one conversation when it is a single defendant. It is a very different conversation when the plaintiff’s lawyer gets to stand in front of the jury and ask who chose this carrier, and the answer points at three companies instead of one.

The insurance problem…limits, exclusions and the fine print

There is a piece of this that almost nobody puts into a carrier or broker risk profile, and it may be the most expensive omission of all. Insurance itself.

Start with a fact that surprises people outside the industry. Freight brokers are not federally required to carry liability insurance. None. A broker is required to have a $ 75,000 surety bond, the BMC-84, and it is worth understanding what that bond is actually for. It exists to ensure carriers and shippers are paid when a broker fails to pay them. It is a payment guarantee. It is not liability protection, and it will not put a single dollar toward a wrongful-death verdict. Kavanaugh flagged exactly this gap in his Montgomery concurrence. Carriers face a federal insurance mandate. Brokers do not, and a 75,000 dollar bond is not liability insurance.

The large brokers carry real coverage. They have buildings, infrastructure, balance sheets, and assets that a plaintiff can actually reach. But the large brokers are not all brokers. A very large share of the brokerage world is mom-and-pop, single-member LLC, pass-through operations with no office, no assets and no liability policy at all. Montgomery made those brokers liable. It did not make them collectible, nor did it give them anything to stand behind. A broker with no coverage and no assets who gets named in a catastrophic case is personally and operationally exposed with nothing between them and the verdict. And when the named defendant has nothing, the exposure does not evaporate. It travels. It lands on whoever else in the chain does have coverage and assets, which increasingly means the shipper.

Now move up to the companies that do carry insurance, because having a policy is not the same as being protected, and this is where risk professionals earn their fee. Two things go wrong. The first is limits. Catastrophic verdicts routinely land in excess of policy limits, and the dollars above the limit do not disappear. Somebody absorbs them. The second, and quieter, one is language. Policies are written documents, and the exclusions, exemptions, sublimits and definitions buried inside them decide what you actually recover, or whether you are actually protected, long after the loss has happened.

I will give you a real one. I worked on a cargo loss involving a piece of oilfield equipment worth about 1.5 million dollars, being moved on an open-deck flatbed carrier. A third-party driver took a turn, the load came off the deck, and the equipment was destroyed. There was a cargo policy in place with a one-million-dollar limit, and on paper, that looked like adequate coverage for the loss. It was not. The policy carried specific exclusions and limitations for open-deck cargo, and open-deck damage of this kind was sublimited to 150,000 dollars. One hundred fifty thousand, against a 1.5 million dollar loss. The shipper, whose equipment it was, absorbed the rest. Nobody read the open-deck language until the claim was already filed.

This is the part the industry treats as somebody else’s problem. Brokers and shippers will tell you they carry contingent auto and contingent cargo coverage, and most of the better ones do. But contingent policies are some of the most heavily conditioned products in commercial insurance. They are layered with triggers, exclusions and definitional language that can keep you from recovering when the freight is yours, or keep you from being protected when you are the named insured. A contingent policy that nobody has ever read closely is one you are guessing about.

So insurance belongs in a risk profile, but not as a yes-or-no field. Whether a carrier, a broker or a shipper carries coverage is the easy question. The real questions are what the limits are against the realistic severity of a loss, and what the language does when a claim is actually filed. That is true of the insurance policy. It applies to the master transportation agreement and the carrier contract. And it is true of the company’s own internal policy manual.

Look at what happened to Werner. The verdict against Werner Enterprises ran near $ 100 million, and it was eventually reversed by the Texas Supreme Court, but only after seven years and a great deal of money spent getting there. Here is the part worth sitting with. That verdict did not come from a compliance failure. Werner was compliant. The case against the company was built on direct-negligence theories, on how it trained and supervised, on the decision to route a trainee, on how its own internal policies and operational guidelines were written and how a plaintiff’s lawyer could characterize them in front of a jury. Compliance did not create that exposure, and compliance could not have closed it. Language did. The wording of policies, contracts and internal documents is risk, and it is risk that lives entirely outside the compliance conversation.

That is why insurers and underwriters retain people like us. Reading a fleet’s loss runs, its policy language, its contracts and its internal policies for the holes, the exclusions and the exposures is a specific discipline. It is fleet risk work. It is what we do for the people who actually make decisions on insurance and litigation, and not a single line of it appears on a SAFER snapshot.

Subcontracting blind spot

There is one more blind spot I want to name, because it is the one that costs people who genuinely believed they did everything right.

I am writing this the same morning I am speaking at a military surface transportation event at Christopher Newport University here in Newport News, and this exact issue is on the agenda. When an organization, a shipper, a broker, or the government contracts a carrier to move a load, it tends to vet that prime carrier and stop. But the prime carrier’s own safety record can be spotless precisely because the prime never touches the freight. It brokers it, or subcontracts it, or hands it down a chain. The real exposure is not the carrier you vetted. It is the carrier you never saw, the one the prime handed it to, and whether the prime even has a subcontracting policy worth the paper it is printed on.

You can vet the prime perfectly and still own the risk of a subcontractor you did not know existed. That is why the no-re-brokering clause, and the question of whether a carrier has a real vendor selection program of its own, are not paperwork details. They are the difference between a vetting decision that holds and one with a hole in the middle, which nobody finds until the crash report comes back with an unfamiliar name on it.

What makes a carrier safe?

This is the wrong question. Not because safety does not matter, it matters enormously, but because safe is a backward-looking outcome, compliant is a minimum floor, and neither one tells you what you actually need to know before you put a carrier on the road with your name attached to the load. The question that does the work is this. What is this carrier’s risk profile? How much exposure does it carry to the motoring public, to its insurer, and now, after Montgomery, to the broker and the shipper who selected it? The companion question, the one a deposition will eventually ask you directly, whether you prepared for it or not: how good is my own process for vetting, qualifying and screening carriers, and would it survive an afternoon of cross-examination?

Carrier vetting for risk exposure is not a SAFER printout. It is a written standard that you follow consistently every time. It is a pre-tender screen that reads FMCSA data correctly and then goes well past it, into financial health, corporate ties, litigation history and catastrophic exposure. It is continuous monitoring instead of a one-time photograph. It is real contract language with a re-brokering prohibition that has teeth. It is reading insurance limits against the realistic severity of a loss, and reading the policy, contract and internal-policy language for the exclusions before a claim finds them for you. It is a driver-level program that treats the federal minimum as a starting line, not a finish line. It is the basic discipline of writing down what you did, because an undocumented good decision and no decision at all look exactly alike to a jury.

I get to be on television and write columns, and I value that but the day job underneath it is this; I am an expert witness in commercial motor vehicle litigation and a loss and risk control advisor to insurers, underwriters and the attorneys who try these cases. Those are the people who taught me, a long time ago, that risk, not safety and not compliance, is where this whole thing actually lives. Tea Technologies, CarrierVerifi and TruckSafe Risk Control exist because that is the work, and because doing it by hand, carrier by carrier, across a dozen separate public databases, is not something a human being can keep up with anymore.

Safe isn’t always exposure-free or risk-free. Compliant isn’t always safe. What “safety” means doesn’t matter and risk is the only one of the three that decides who pays.

I work for a publicly funded truck driving school. Are there any better resources than SAFER for drivers to screen potential employers?