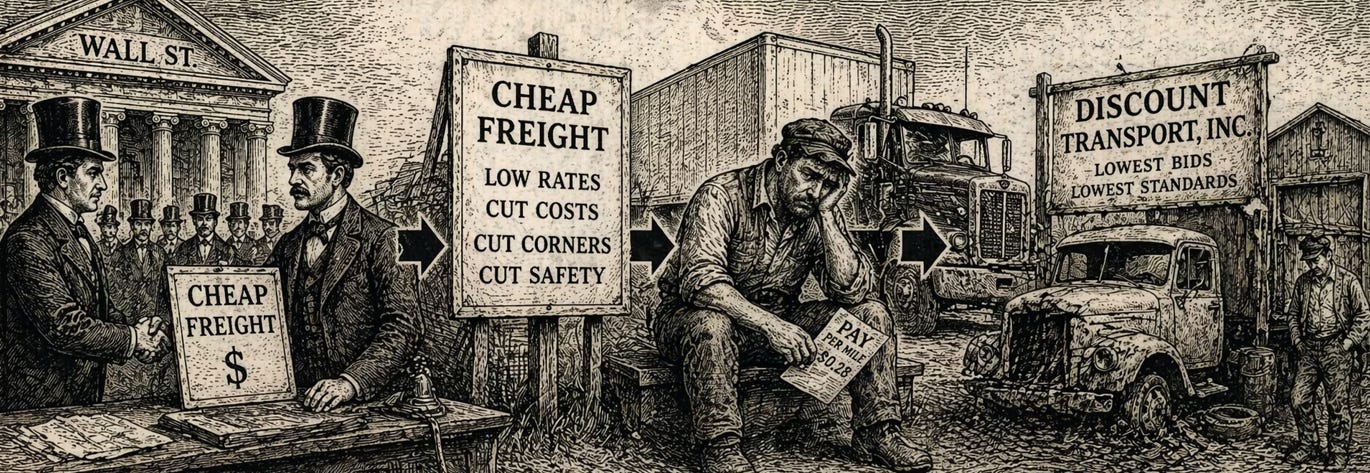

The Freight Economy Built on Cheap Stuff Is Producing Cheap Carriers

Broker, shipper and carrier relationship data shows 64 fatalities, carriers with multiple FMCSA BASICs in alert status still hauling loads. That's the reason we did 60 Minutes and CBS News segments

No single piece of this explains how we got here. It is all of it together. The freight that does not pay enough to attract qualified carriers. The brokers who screen by checking three boxes. The bonds that run out by claimant 23. The carriers who cycle identities and keep rolling. The data that exists is public and gets ignored. A Supreme Court case awaits a decision that will determine whether moving freight through the cheapest available carrier on a load board carries any accountability at all when someone dies.

Start with a man in Tennessee. He runs one truck. Has been running it for 12 years. He found a load on DAT from a broker he had not used before. The rate confirmation looked legitimate. The load paid what he needed it to pay. He picked it up, ran it through the cleaning process, delivered on time, received a signed proof of delivery, and submitted his invoice.

Thirty days later, nothing. Forty-five days, still nothing. The calls went to voicemail. The emails bounced back. He checked SAFER and found out the broker’s operating authority had been revoked two weeks after he delivered. He filed a claim against the $75,000 surety bond because that is what the bond is intended to cover. He was claimant number 47. The bond was already exhausted. He received a $312 check.

That is what the freight broker financial responsibility system produced for a 12-year professional who delivered on time and documented everything. Three hundred and twelve dollars.

That story actually begins much earlier, with a freight economy that has been systematically rewarding the cheapest possible transaction for a decade and an industry structure that converted almost every accountability mechanism into a checkbox. To understand where we are, you have to trace the full chain, from the consumer buying cheap goods and expecting free delivery, to the broker sourcing the cheapest possible carrier for the freight, to the carrier that can only afford to haul at that rate because it has compressed every cost including safety, to the bond that runs out at claimant 23, to the Supreme Court case awaiting a decision that will tell us whether anyone in the middle of that chain has to answer for what happens when the truck crashes.

The structural cause of cheap freight is not a mystery. GLP-1 medications, Ozempic, Wegovy, Mounjaro and the growing class of appetite-suppressing drugs have now penetrated more than 16 percent of American households. KPMG estimated that users cut caloric intake by 21 percent and reduced monthly grocery spending by 31 percent, a projected $48 billion annual reduction in food and beverage spending through 2034. The CoreLogic analysis and DAT reefer data have tracked the resulting freight impact, potentially totaling 450,000 fewer truckloads per year at current penetration rates. Del Monte Foods declared bankruptcy in 2025, citing a 4 to 5 percent decline in packaged food demand. The food freight that has always been the backbone of refrigerated truckload volume is compressing in ways that are structural and accelerating, not cyclical.

At the same time, a decade of ultra-cheap imported goods conditioned millions of American consumers to expect products to cost almost nothing and to ship for free. Large retailers with enormous logistics leverage drove shipping costs as close to zero as possible at the consumer-facing level, suppressing the market signal that tells the supply chain that moving freight over long distances costs real money. When that signal is suppressed at the consumer level, it is suppressed everywhere downstream. Shippers negotiate accordingly. Brokers find carriers accordingly. Carriers bid accordingly.

The SONAR Outbound Tender Volume Index and the extended contract rate compression documented in FreightWaves data throughout 2023 and 2024 tell the quantitative story. Carriers were receiving spot rates in nominal terms roughly equivalent to 2014 peak rates, while ATRI data shows operating costs had risen approximately 34 percent since 2014. The industry lost tens of thousands of carriers in 2023 and 2024, according to FMCSA authority data. The survivors disproportionately had the lowest cost structures. Some of that reflects legitimate efficiency. Some of it reflects the compression of driver pay, driver qualification, maintenance investment, and insurance quality to levels that the professional trucking industry should find alarming.

At the absolute bottom of the freight value chain, below low-value freight, is no-value freight. Garbage. Municipal solid waste. Scrap. Materials with zero commercial worth. This category not only attracts the worst carriers but also operates in a regulatory space where normal accountability structures do not apply. Under 49 CFR Part 371, broker authority requirements apply to arranging transportation of property with commercial value. Certain exempt commodities, including categories of solid waste, have historically fallen entirely outside the broker authority framework. You do not need federal broker authority, a surety bond, or FMCSA registration to arrange the movement of trash between carriers. The accountability chain that broker regulation creates in the legitimate freight market simply does not exist in the exempt commodity space. Those carriers operate at highway speed and full weight alongside everyone else.

The spot market broker system actually produces an absolutely toxic carrier pool. The bottom feeders of the industry.

Tea Technologies, through its Highway Intelligence and Risk Platform, aggregates FMCSA inspection and crash data from carrier bill-of-lading records captured during roadside inspections. When a carrier gets inspected with a load on board, the inspection record captures the broker, the shipper, and the carrier in a single data point. It is not self-reported. It is what enforcement officers found when they stopped the truck. THE TEA analysis of carrier history data for CH Robinson and Total Quality Logistics, the two largest freight brokers in the country, covers 1,730 carriers across the two datasets. This is what that data shows.

CH Robinson manages 37 million shipments annually and works with 450,000 contract carriers, according to its own description. The TEA carrier history dataset documents 923 carriers with inspection records in the system. Of those 923 carriers, 30 had fatal crashes in the past 24 months, producing 46 fatalities. Seven hundred of 923 carriers (76 percent) have never received an FMCSA safety rating because they have never been subject to a compliance review. One hundred thirty-two have vehicle out-of-service rates at or above 50 percent. 74 have driver OOS rates at or above 50%.

TQL’s carrier dataset covers 807 carriers. Seven had fatal crashes in 24 months, producing 18 fatal crash events and 18 confirmed fatalities. Eighty-five carriers had at least one crash. Ninety-one percent of TQL’s carrier base, 731 carriers, have never been rated by FMCSA. One hundred forty-three have vehicle OOS rates at or above 50 percent. One hundred fifty-four have driver OOS rates at or above 50 percent. TQL has 44 carriers in its documented load history carrying an authority transfer flag from THE TEA’s cross-reference analysis, indicating patterns consistent with a prior entity operating under a new identity. That is more than seven times the six authority transfer flags in CH Robinson’s carrier base and represents a significant concentration of chameleon carrier risk inside a single broker’s documented carrier pool.

In CH Robinson’s carrier history, Twin Carrier LLC out of Georgia, DOT 3518735, has had 62 crashes in 24 months, two of them fatal, two people dead. Three simultaneous SMS alerts. Unrated. $1,000 coverage, canceled. Also in CH Robinson’s carrier history. Twin Carrier is the primary and one of the oldest Super Ego network carriers, which also has two wrongful death murder cases pending in Pennsylvania and Ohio by two different drivers.

Koleaseco Inc out of Michigan, DOT 667715, carries 13 crashes in 24 months, one of them fatal, with four people killed in that single crash event. Rated satisfactory on a prior review from FMCSA.

Clement Transport LLC, out of New Jersey, DOT 3371628, has had 20 crashes, one fatal, two people dead. One hundred percent Hazmat OOS rate, 24% driver OOS rate, and a 38% vehicle OOS rate, meaning every driver this carrier has had pulled from the road during roadside inspection. Every single one was put out of service after a hazmat inspection. Also in CH Robinson’s carrier history.

Cobra Inc out of Pennsylvania, DOT 3525693, 30 crashes, one fatal. Unrated. The insurer listed is Universal Casualty Risk Retention Group, a risk retention group that is a systemic concern in the commercial trucking insurance market. An RRG insuring a carrier with 30 crashes.

Contract Freighters Inc., out of Missouri, DOT 70289, is one of the larger operations in the dataset with 104 crashes in 24 months, four of them fatal, four dead. A satisfactory safety rating.

There is a mechanism that makes all of this possible, and the legal question that determines whether it changes remains open.

In most spot-market brokerage operations, verifying a carrier for a load typically follows this process. Confirm the DOT number exists in SAFER. Confirm the MC number is active. Confirm that a certificate of insurance is on file. Confirm they’re not rated Unsatisfactory or Conditional by FMCSA. That is it for many operations. It checks that the carrier is technically permitted to operate, which is a different thing entirely from checking whether the carrier is safe to operate, ensuring your carrier’s freight arrives safely between origin and destination. There’s also the fact that a large portion of US carrier fleets have no rating at all and remain “unrated.” For most brokers, when selecting a carrier for a load, a rating and an authority that can be purchased for as little as $1,200 are good enough. A carrier can pay $300, rent a rental truck, get some self-attested, non-underwritten, instant issue coverage, and you’re a trucker.

The reason this three-box process is standard in much of the spot market is exactly what the Supreme Court is currently deciding.

On March 4, 2026, the Supreme Court heard oral arguments in Montgomery v. Caribe Transport II, LLC. Shawn Montgomery was parked on the shoulder of Interstate 70 in Illinois on December 7, 2017, when a CH Robinson-hired carrier struck him at highway speed. He lost his leg. He sued CH Robinson on a negligent hiring theory, arguing the broker selected a carrier with known safety problems. Lower courts dismissed the claim, ruling that the Federal Aviation Administration Authorization Act of 1994 preempts state-law negligence claims against freight brokers because carrier selection is a core broker service within the FAAAA’s preemption scope. CH Robinson argued to the Supreme Court that brokers should not face state liability because they do not own or operate the trucks and because state liability patchworks would undermine the uniform federal transportation framework. The U.S. government filed a brief in support of CH Robinson. Montgomery’s attorney, Paul Clement, argued that Congress designed the FAAAA to deregulate economics, not to eliminate state safety tort law, and that the safety exception specifically preserved these kinds of claims.

TQL is not simply watching from the sidelines, because the Sixth Circuit’s decision in Cox v. Total Quality Logistics was directly cited in the legal analysis of the circuit split that brought this case to the Supreme Court. TQL is materially affected by whatever standard the Court establishes. A decision is expected by the end of June.

If preemption holds, there is zero legal downside to putting Kooperativ LLC on a load while it has four SMS alerts and $750 in canceled insurance. Confirm the DOT. Confirm the MC. Confirm the certificate. Move the freight. Collect the spread. If someone dies, the carrier’s minimum insurance covers what it can, and the broker’s exposure is gone. Check the three boxes. Cash the check.

If the safety exception survives and negligent hiring claims proceed under state law, a broker that put a bad carrier on a load while Tea Technology was showing 300+ crashes and eight fatalities and a high alert risk score will face a very uncomfortable conversation about what it means to exercise due diligence when data tools exist, are publicly available, and were not consulted. Accountability creates incentive. That is the entire theory of tort law. It is why the brokerage industry has invested so heavily in the preemption argument.

The CBS 60 Minutes investigation that aired April 12 documented the Super Ego Holding network, a Serbia-connected operation that FMCSA Administrator Derek Barrs called one of the most notorious chameleon schemes on American highways. I contributed to that investigation. What Bill Whitaker and the CBS team documented was not an anomaly. It was a visible example of a systemic condition. Drivers being told to physically alter DOT numbers on truck doors. Rate confirmations are being fraudulently modified to cut driver pay by $700 per load. Eighteen-hour shift demands. Throughout it all, freight is moving because someone in a broker’s office confirmed three things on a SAFER screen and booked the load.

The bond system, which is supposed to create financial accountability when brokers fail, is inadequate by the numbers and by history. The $75,000 requirement was set in 2013 by MAP-21 after sitting at $10,000 for 40 years. When MAP-21 raised it, more than 7,500 brokerages closed because they could not get bonded at the higher amount. $75,000 still does not cover what it needs to cover. A broker handling 50 loads a month can easily carry $100,000 or more in outstanding carrier payables at any moment. When that broker collapses, the $75,000 is divided among all claimants. FMCSA data shows more than 400 brokers experience bond drawdowns annually. Nearly one in five has total claims exceeding the bond. The average recovered amount is around $1,900, and the reason that number is so depressed is that carriers have learned that filing against an exhausted bond produces $312 checks.

The fraud layer makes it worse. Double-brokering and identity-fraud operations buy old MC numbers with clean histories, spoof phone numbers, run a few weeks of loads without paying carriers, then dissolve and reappear under a new identity. The surety bond on the fraudulent operation may have been written against an entity that barely existed. The trail ends with whoever made the phone call.

If you are a small carrier or owner-operator running spot freight, there are things you can do that the regulatory system will not do for you. Verify broker authority on SAFER before you pick up the load, not after. Understand that the $75,000 bond is a last resort that may already be pledged against 46 other carriers in the queue. Trade credit insurance deserves serious consideration. Companies like Allianz Trade, Coface, and Atradius write accounts receivable insurance that pays 80 to 90 percent of an invoice if the broker defaults. Premiums run roughly 0.2 to 1 percent of insured receivables, depending on volume and claims history. Some freight factoring companies bundle credit protection into their non-recourse factoring programs. Ask specifically about that option. It is not free, but it is substantially better than waiting six weeks for a $312 check.

Build shipper-direct relationships wherever you can. The structural difference between contract freight with an established shipper and spot freight from an unknown broker on a load board is the difference between a business relationship you understand and extending credit to a stranger. Not always available. Not always practical. But worth pursuing deliberately, especially in a market environment where spot market broker fraud is running at documented historic levels.

For every compliance manager, fleet safety director, and carrier qualification team working for a shipper or larger motor carrier, the data in this article is a call to action. The carrier qualification tools exist. THE TEA, Highway, Searchcarriers, Blue Wire, Genlogs, the FMCSA SMS system, SAFER, crash history, OOS rates, authority transfer indicators, and insurance verification beyond confirming a certificate exists; these are not exotic or expensive tools. They are available. The question the Supreme Court is answering is whether there is a legal consequence to choosing not to use them when the carrier you hired kills someone.

The answer arrives by the end of June. Nine justices will determine whether the people who select the carriers bear any responsibility for who they select. If the answer is no, the spot market continues to operate exactly as reflected in the data in this article; some carriers, with 300+ crashes and 8 fatalities, remain carriers someone puts on a load. If the answer is yes, every broker in the country will soon reconsider what carrier vetting looks like, and the three-box process will need to become substantially more serious.

The Tennessee owner-operator with his $312 check already knows which answer would have helped him. The families represented in those 64 fatalities documented across two brokers’ carrier histories probably have a view on it too. The people driving vehicles on American highways alongside trucks operated by carriers with canceled insurance, multiple BASIC alerts, and a driver who failed his last roadside inspection deserve to know that someone is asking these questions, even though a June ruling will answer them.